Key Points:

- S&P 500 valuations in the 94th percentile of all time

- Equity risk premium near zero — levels seen before 1987 and 2000 crashes

- Pimco warns of increased downside risk if negative shocks hit

- Bonds may outperform stocks in the years ahead

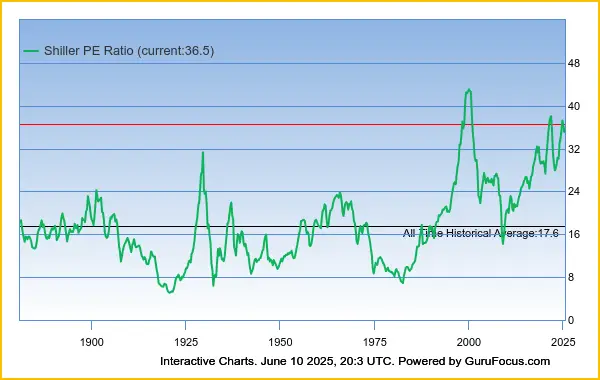

S&P 500 Valuations in the Danger Zone

Equity valuations have climbed to levels “historically seen before big corrections,” warned bond giant Pimco in a note penned by Richard Clarida, Andrew Balls, and Dan Ivascyn. Using two key indicators, the $2 trillion asset manager pointed to mounting risks facing the market today.

The Shiller cyclically-adjusted price-to-earnings ratio (CAPE) — which compares current S&P 500 prices to a 10-year moving average of earnings — is currently around 36x earnings, placing it in the 94th percentile of all-time readings.

“A mean reversion to a higher equity risk premium typically involves a bond rally, an equity sell-off, or both,” the note said.

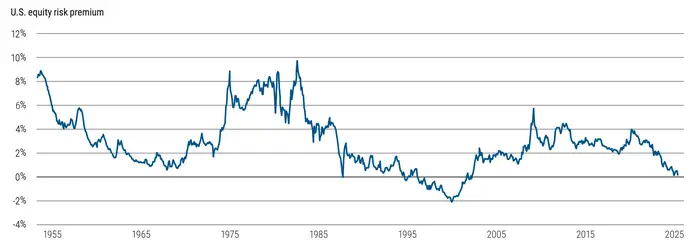

Equity Risk Premium at 1987 and Dot-Com Levels

Alongside CAPE, Pimco flagged the equity risk premium (ERP) — which measures expected stock returns over 10-year Treasurys — as another red flag. Currently sitting near zero, this level has been matched only 10% of the time historically.

The note continued:

“The same chart shows two prior times when the premium was zero or negative: in 1987 and in 1996–2001.”

In both cases, what followed were brutal corrections:

- September 1987: After ERP hit zero, the stock market plunged 25%, and 30-year real bond yields fell 80 basis points.

- December 1999: ERP reached its lowest point of the period; what followed was an equity drawdown of nearly 40%, ending in February 2003. Over that same stretch, 30-year real bond yields dropped about 200 bps.

Bonds Could Outperform Stocks Going Forward

With stock valuations stretched, Pimco suggests fixed-income assets might be the better play. The firm noted:

“High stock valuations make it likely that fixed-income assets outperform stocks in the years ahead.”

Investors can currently benefit from high yields, and with rate cuts possibly on the horizon, there’s potential for both attractive coupon income and bond price appreciation.

Vulnerability to Shocks

While Pimco admits that valuations alone do not predict short-term market moves, they amplify risks in the face of bad news.

“If a negative catalyst comes along — a bad jobs report or rising inflation — high valuations leave the market vulnerable to more pronounced downside.”

Calm Before the Storm?

Despite a recent stretch of calm in the markets as investors await the effects of President Trump’s tariff policies, Pimco’s analysis suggests that this tranquility may be fragile. The metrics cited point toward a market that could react severely if sentiment shifts.

Source: Pimco economic commentary, June

Levi’s Jeans Discount